Economic Research Report: The Fed is All Mixed Up

If the Federal Reserve were paying close attention to the money supply it would know that monetary policy is now tight. Through April, the narrow M1 measure of money has fallen for thirteen straight months. The broader M2 measure of money has dropped nine months in a row and is down 4.6% from a year ago. M3, a broader measure of money that includes large CDs, is down 4.1% from the peak last July. Meanwhile, bank credit at commercial banks as well as their commercial and industrial loans are both down. If this isn’t tight, we’re not sure what tight means.

It remains to be seen how quickly these reductions in the money supply will translate into inflation getting back to the Fed’s 2.0% target, but the Fed has gained some traction against the inflation problem. And yet, once again, the Fed uttered not one peep about the money supply in its policy statement, nor did any journalist broach the topic.

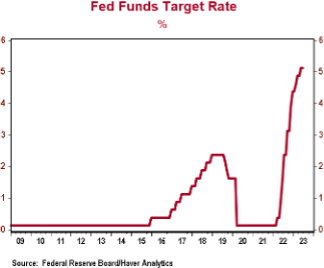

Instead, the Fed remained focused on its target for short-term interest rates, which it decided to keep unchanged in the 5.00 to 5.25% range, like the consensus expected. Oddly, however, at the same time that it decided not to raise rates it decided to amend the “dot plot” to show two more quarter- point rate hikes later this year. It also changed the language in the policy statement to make it clear it’s looking for more information to decide how much to raise rates later this year, not whether to raise rates later this year. Notably, no one on the FOMC – the Fed’s rate-setting committee – predicted a rate cut this year.

In one way, this makes sense: the Fed is now forecasting better economic growth and lower unemployment this year than it was back in March, so a higher peak rate makes sense. But if the Fed expects to raise rates twice later this year, why not raise them at least once today? Fed Chairman Powell noted at the press conference that core measures of inflation remain stubbornly high, suggesting the Fed is discounting recent lower readings on headline inflation, which have been largely driven by lower energy prices. So, again, why not raise rates today?

Perhaps the worst part of all this is the Fed’s decision was unanimous: not one member decided the mix of the statement, the dot plot, and the lack of action didn’t make sense. The Fed is all mixed up. The reason it’s mixed up is because in the 2008-09 crisis it abandoned its long tradition of implementing monetary policy through scarce reserves and imposed a new policy based on abundant reserves. We think a quarter-point rate hike is likely in July. But whether we get more than that will depend on how quickly the reductions in the money supply that the Fed is ignoring effect the economy later this year.

Text of the Federal Reserve’s Statement:

Recent indicators suggest that economic activity has continued to expand at a modest pace. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5 to 5-1/4 percent. Holding the target range steady at this meeting allows the Committee to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.

—

This was written by:

Brian S. Wesbury, Chief Economist, First Trust

Robert Stein, Deputy Chief Economist, First Trust

This report was prepared by First Trust Advisors L. P., and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subjet to change without notice. This informaton does not constitute a solicitation or an ofer to buy or sell any security.

Share this article